The Economy, Brought to you by the Letter “K”

Image source: The Onion

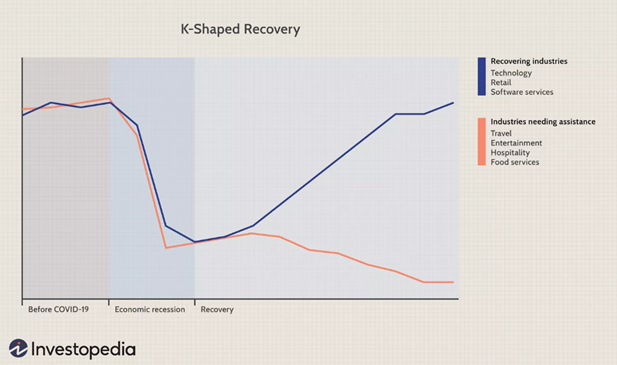

During the latter part of 2025 and the beginning of 2026, many economists were predicting a “K” shaped economy, and again the investing public was presented a term they may not have heard of. Morgan Stanley defines a K-shaped economy as an uneven economic recovery or growth pattern where different sectors or income groups diverge sharply, with some rising while others decline or stagnate. It signifies widening wealth inequality, often with high-income earners and technology sectors thriving while lower-income households and specific industries struggle. Simply put, this can show a growing disparity between rich and poor.

A lot has changed since this prediction due to special circumstances like the Iran War and the special nature of the U.S. president. In the chart below, we see that the “K” involves high-growth industries like technology that move higher while industries like consumer discretionary move lower. With oil prices spiking due to the Iran War, it is a near certainty that all businesses will be negatively affected, a new black line will appear and will move higher; the black line representing energy, specifically oil.

The impact of high oil prices can be felt differently by consumers depending on whether the prices are high because of a strong economy or if they are high because of supply disruptions, also known as a “negative supply shock.” The reason high energy prices are not as negative during a strong economy is that part of the higher energy prices can be absorbed by the stronger earnings potential of individuals and businesses. The impact of a negative supply shock can be high inflation, reduced consumer spending, higher interest rates, lower bond prices and potential recession. Incomes and revenues go down and the ability to pay the higher prices is diminished.

We pointed out in our last article that news changes very fast and what we think we know today might change tomorrow. Because of this we try to show long-term trends driven by recent events to give insight into how we make investment decisions for our clients and allow the portfolio to be durable and investors to endure. As oil prices increase due to disruptions in supply, more alternative energy is being adopted, immediately in the form of EV sales and solar installations. These are only the immediate effects of the Iran War. The increased interest in nuclear power generation will almost certainly accelerate and the long-term trend of energy production from oil will continue to decline. Long-term trends from this negative supply shock can also lead to lasting behavioral changes from the consumer (traveling less), from business (reduced innovation) and from government (tax and spending changes).

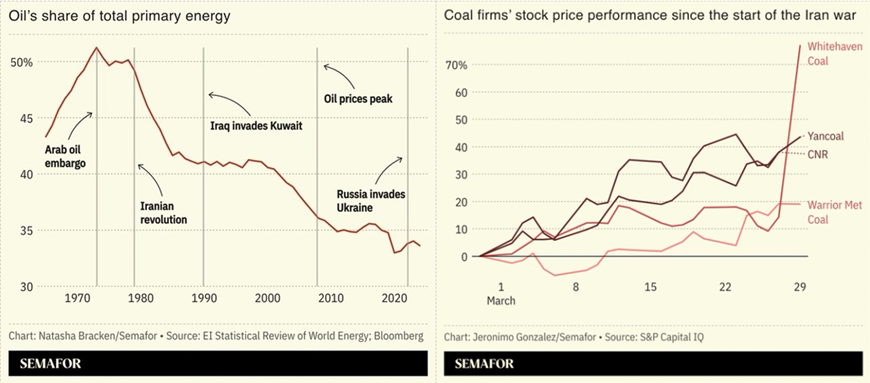

This is not to say oil is going anywhere… it isn’t. Countries like Canada and Norway are trying to increase oil production and exports. It is also important to note that about 14% of the world’s oil consumption is used for non-energy purposes. While the percentage of global energy generation from oil is dropping, its production continues to increase. According to the International Energy Agency (IEA), crude production total in 2023 was just over 190 billion barrels and increased 22% from 2000 to 2023. We are also seeing a short-term increase in demand for coal, implying that this won’t necessarily be an alternative energy boom, but a rush to energy generation of all kinds to meet global demand if oil supply stays disrupted for longer than expected.

What hasn’t changed is the portfolio construction of our positions in high-quality companies and a higher-than-normal position in money markets. We are continuing to trim profits and reinvest, at least partially, in high quality companies that have sold off for various reasons but that still have strong business fundamentals. What has changed is the removal of some individual positions that have outsized economic risk or management teams that are slower to adapt to a changing economy. We have also moved into industry and geographic indexes where stock picking becomes riskier. This allows us to participate in a rising asset class, like oil, without risking picking an individual company that could have exposure to a geographic location with higher risk than necessary.

This type of risk management allows the portfolio to be less volatile during times of high uncertainty and have a quicker recovery when conditions improve. This allows us to replace the “K” with ZZZ because the sleep-at-night factor is critical in risk management.

This newsletter has been prepared by Stephen Maser of Raymond James Ltd. (“RJL”). It expresses the opinions of the writer, and not necessarily those of RJL. Statistics, factual data and other information are from sources believed to be reliable but accuracy cannot be guaranteed. It is furnished on the basis and understanding that RJL is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. RJL, its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. This provides links to other Internet sites for the convenience of users. Raymond James Ltd. is not responsible for the availability or content of these external sites, nor does Raymond James Ltd endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd adheres to. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Raymond James Limited is a Member Canadian Investor Protection Fund. Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd., member FINRA/SIPC.