The Aimless Bull Market

Image Source: The Hollywood Reporter

Do you ever get the feeling that you should be worried even if everything is going along just fine? Some sort of intuition is warning you to be cautious, but you can’t articulate why? If you are following the market, odds are you might have this feeling. We believe we can help pinpoint this sense of financial anxiety, as there is a trifecta of contradictions in the current market that we feel are related to each other: the IPO of SpaceX, the price of energy and the artificial intelligence race. And we’ll show you that you can survive this anxiety with your portfolio intact.

First, the SpaceX initial public offering (IPO), specifically the valuation when it came to the public market. SpaceX's (SPCX) IPO raised over $75 billion at a valuation of approximately $1.77 trillion, making it the largest market debut in history. The offering bundled SpaceX’s aerospace business, Starlink, xAI and X (formally known as Twitter). All this for a business that reported $18.7 billion in consolidated revenue last year but lost nearly $5 billion. Basically, you have one profitable business (Starlink), wrapped up with one that could become profitable (SpaceX) and two losers that burn a pile of cash so large you could see it from space. The IPO also had a restricted float of under 5% of total outstanding shares, creating an artificial scarcity. Of 19 analysts who follow SPCX, Keith Snyder, senior equity analyst at CFRA has the only “sell” recommendation for SPCX. This is compared to all the other major analysts who rate this company as a “buy”, most of whom were part of the underwriting effort. It should be noted that CFRA is not an investment bank. Full disclosure, our parent company, Raymond James Financial (RJF) was one of the named investment banks for the SPCX IPO but our team feels this is a highly speculative buy. This goes to show the independence RJF shows its advisors in allowing us to point this out.

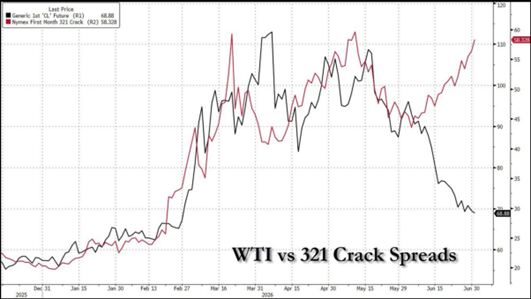

Second, there is a disconnect between the futures price of oil, the delivered price of oil and the price of oil’s refined products. On July 2, oil expert Matt Randolph spoke about the West Texas Intermediate (WTI) oil price versus the 321 Crack Spreads. The 321 Crack Spread shows the profit margin of refiners (3 barrels (bbl) of oil create 2 bbls of gasoline and 1 bbl of diesel fuel, hence 321). The spread is at an all-time extreme because gasoline and diesel inventories are very tight. One of two things can change this: either oil prices go up or petrol prices come down.

The futures price of oil and the physical delivery price are also at a large spread (delivery price is on average $20/bbl higher), a price gap that is usually much closer to each other. Part of this problem, as Randolph sees it, is that the price of oil has dropped because the markets are being manipulated by the on-again, off-again nature of the Iran War. Oil demand has also risen as China is buying more oil at lower prices, when it would typically be higher in such a volatile environment. No one can predict what the state of geopolitics is going to be tomorrow, let alone in three to six months, but Randolph is certain that this gap will correct itself and he thinks the futures price will move upward to meet the delivery price. Even with all of this happening in the oil markets, it’s taking a back seat to the artificial intelligence trade.

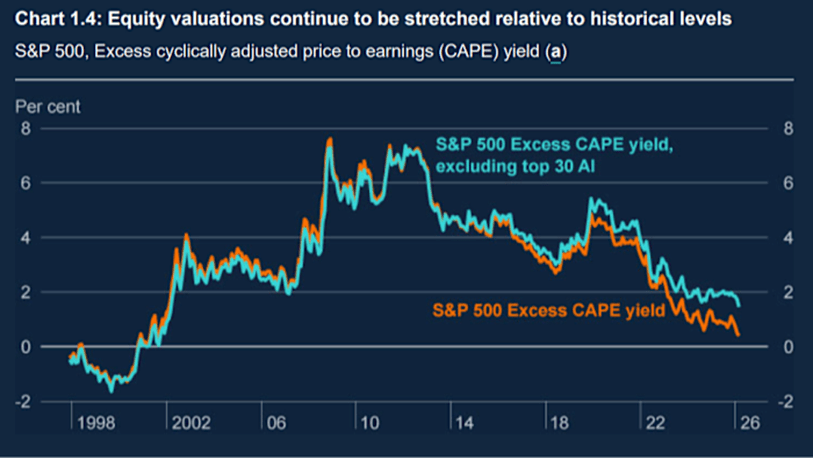

This brings us to artificial intelligence and the companies that are building this technology. In his July 8 newsletter, Daire MacFadden from the Financial Times discussed the high valuations in tech. A chart from the report shows the S&P 500’s excess Cape yield – cyclically adjusted price-to-earnings yield minus the real bond yield, a measure of how expensive stocks are.

Source: The Financial Times

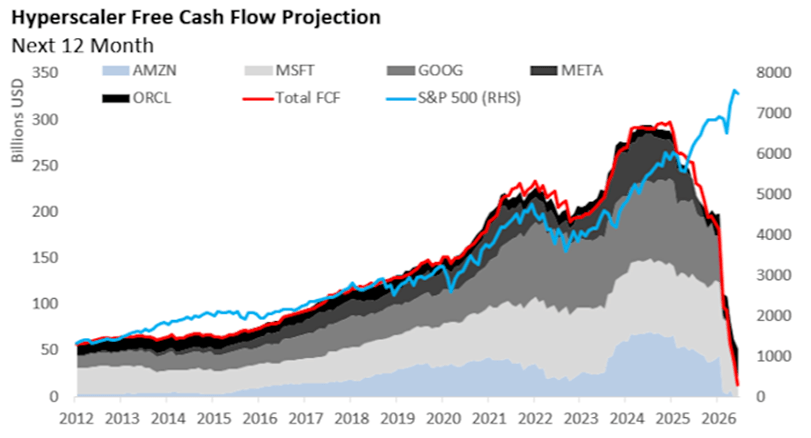

Simply put, if the yield is falling, stocks are becoming more expensive in relation to other assets. The chart shows they’re nearing dot-com era levels. MacFadden goes on to say that these valuations are only half the story when you look at the hyperscalers’ free cash flows, as that money is going to capex to build AI infrastructure, like datacentres.

Source: The Financial Times

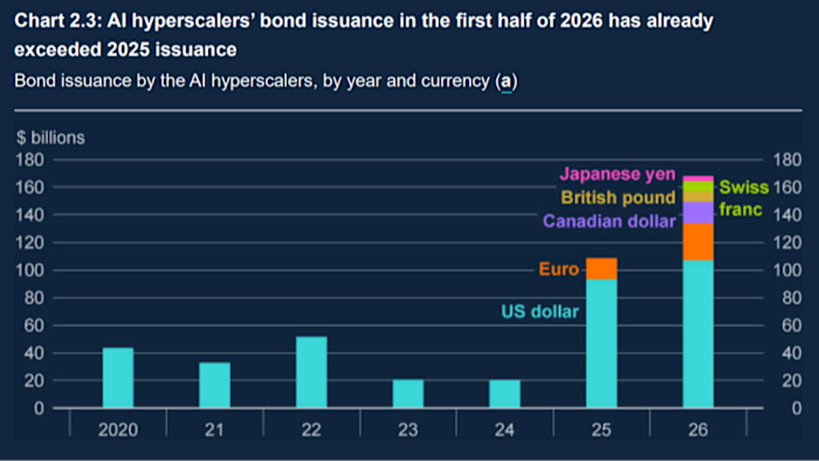

These capex needs are now exceeding present-day profits. To close the gap, the hyperscalers have turned to global debt markets.

Source: The Financial Times

Combined with this financial data, Meta is now going to sell their excess compute. The question is, “Sell it to whom?” The biggest frontier labs (Alphabet, OpenAI, Meta and Anthropic) are using the vast majority of this compute. We need to ask what happens when Meta starts selling compute they themselves can’t use. We also need to ask ourselves how much future compute demand there is. And finally, they need to figure out how to make more money than they spend and this is not yet obvious. Ed Zitron calls this the mirage of demand.

OpenAI has delayed their IPO into 2027, as their goal was to go public with a trillion-dollar market cap. This might be hard to do with no path to profitability and when SpaceX, Alphabet and the debt markets are swallowing up capital. The massive spending programs in artificial intelligence and the returns needed to justify these capital expenditures are not clear. Zitron’s newsletter from June 30 states that 60% of organizations are token minimizing. It’s a long read and worth the perspective but simply put, firms can’t afford to use AI because the cost of use is more expensive than the workers it’s supposed to replace.

This information is not meant to make you think the sky is falling, as momentum for the market is clearly trending upwards. What we are trying to show is the potential warning signs, why this bull market will not last forever and how we intend to avoid undue financial damage to portfolios. This data is also primarily focused on the U.S. economy and markets. Obviously, what happens to the U.S. affects the world economy, but there are areas to watch and potentially take advantage of, and for Canadians and investors in Canada, there’s reason for optimism.

The first thing to note is the July 1 deadline to renew CUSMA has come and gone due to the holdout of the Trump administration. However, despite the headlines that imply otherwise, Capital Economics points out that this changes little in the near term, as the agreement will remain in place until 2036, subject to annual joint reviews. I encourage the full read of this article from The Globe and Mail for better context. The U.S. dollar is also high, in comparison to the Canadian dollar. Energy is volatile and there have been historical evidence that the Canadian dollar and Canadian-dollar-denominated equites have done well in this kind of environment.

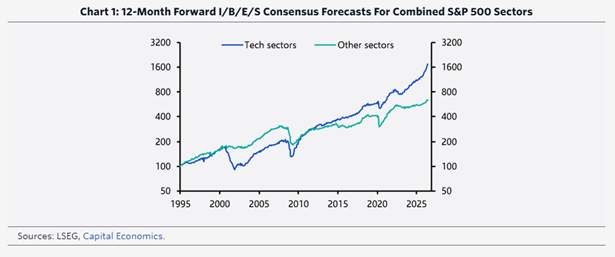

Capital Economics does not believe we’re at the end of the AI run either, and what’s true of all potential bubbles is that you have no idea when they can pop. As well, the tech run-up is fueled by earnings despite their massive AI spend.

This is why you need to be nimble and take profits when you can. We’ve been active in taking profits from our U.S. holdings, particularly in tech, and moving some of that capital back to Canada. Our consistent “buy, hold and rebalance strategy” doesn’t mean we’re eliminating tech, but we’re aware of the potential future risks associated with them. We continue to have a good reserve of cash for opportunistic buying and we’re careful buying into the AI investment “hopium”. It can get you crushed when the bull turns into a bear and finds you in its path.